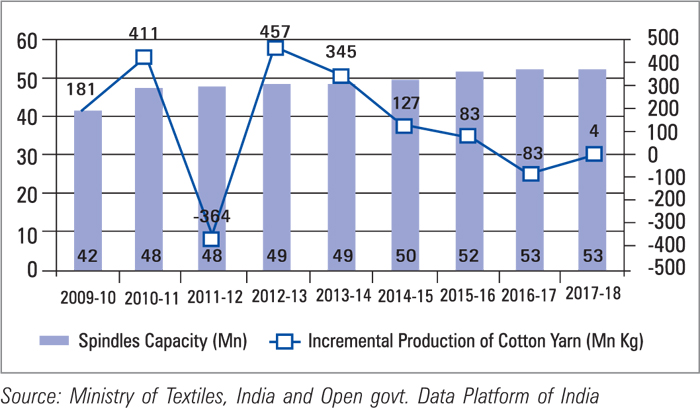

The Indian Spinning sector is on the throes of a big crisis. It is dogged by excess spindelage capacity which remains unutilised leading to losses. This is because the domestic demand and export outlets are not supportive to absorts the excess capacity in the industry. Thus over the last decade the exportable surplus of cotton yarn has increased to about 27 per cent in 2017-18 as per the latest official data.

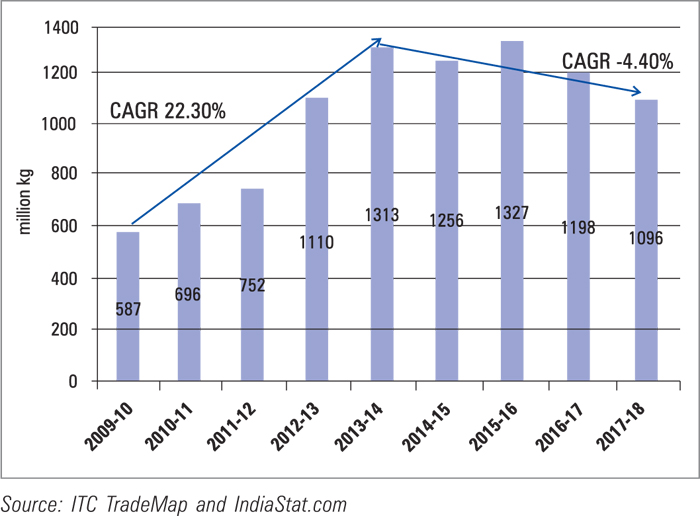

How to siphon off the surplus? The way out is exports. For that, the industry needs incentives which were withdrawn after 2013-14. It is clearly struggling despite having the world’s largest spinning infrastructure and the capability to produce the fine quality yarn in the world. The withdrawal of incentives has meant a substantial decline in exports between 2013-14 and 2017-18 at a CAGR of 4.4 percent. Prior that exports increased at a CAGR quantitative of 22 percent during 2009- 2010 to 2103-14.

In value times, exports declined by 25 percent from @4570 mn in 2013-14 to $3443 mn in 2017-18 because of disadvantages faced by Indian exporters in the global market. China, the largest importer of Indian yarn, has shifted to Vietnam or Indonesia where it has duty free access, while Indian yarn attracts a 3.5 per cent duty. The other major export distination are Bangladesh, Pakistan, Egypt, Portugal and Korea. On the other land, exports from Vietnam and Indonesia have increased at a remarkable rate of 129 percent and 55 percent respectively in the same period.

Cotton yarn contributes significantly to India’s exports basket with $3.80 bn (estimated value) in 2018-19, about 10.55 per cent of the total textiles and apparel exports during the same year. India also faces challenges in the global market vis-à-vis competing countries. Indian yarn exports are subject to a 4 per cent duty in the European Union (EU), while Vietnam and Indonasia levy a 3.2 per cent tariff. Least – developed countries get duty free access.

The spinning sector also suffers from low cotton yield, contamination, high moisture content and increasing cotton prices during the loan cotton supply season. Besides, there is a decline in the margins of the spinning industry due to price gap of cotton yarn over cotton, high manufacturing cost due to high interest rate and power tariff, pending TUFs claims, says CITI economic desk.

The CITI desk suggests that the entire cotton textiles and apparel value chain needs concerted efforts by all stake holders for its substainability and growth. Cotton yarn and fabrics should be covered under the scheme for Rebate Of State and Central Levies (ROSCTL) so as to take care of embedded taxes and impart competiveness to the spinning industry.

With surplus production many spinning mills are working six days a week or working at 70 to 80 per cent capacity utilisation only, one of the lowest in the history of 40 years. There is also need for extension of the three per cent interest equalisation scheme to textiles and apparel sector, exemption from cross power subsidy surcharge, direct subsidy to cotton farmers, formulation of industry- favourable free trade agreements as well. Other WTO compliant export incentives to cotton yarn and fabrics to create a level plying field for Indian exporters are also called for.

For most spinning mills, margin levels have dropped significantly in the last few years compared to movement in revenue. On an average spinning mills revenue has increased at a CAGR of two per cent in the last five years. However, earnings before interest, taxes, depreciation and amortization margin has declined at a CAGR of more than 8 per cent, says CITI Economic desk.

For most spinning mills, margin levels have dropped significantly in the last few years compared to movement in revenue. On an average spinning mills revenue has increased at a CAGR of two per cent in the last five years. However, earnings before interest, taxes, depreciation and amortization margin has declined at a CAGR of more than 8 per cent, says CITI Economic desk.

Further, the gap between change in the cotton prices and yarn prices have declined after 2014 which however marginally improved in 2018. Yarn prices do not increase in the same lines as cotton as demand for yarn is always over shadowed by higher supply. This gap has meant a raise in the working capital for the mills and decrease in their margins. An increase in the global cotton prices leads to an increase in Indian prices also, but a decline in the world cotton prices is not noticed in India due to high minimum support price (MSD) of cotton.

As is known, the manufacturing cost of cotton textiles in India is comparatively higher than that in Bangledesh and Vietnam. The power cost in India is US cents 10-12 per cent Kwh While it is US cents 9-12per Kwh in Bangladesh and US cents 8 per Kwh in Vietnam. In India the interest rate is 12-13 per cent. Which it is 6-7 per cent in Vietnam, 10-12 per cent in Turkey and 5-6 per cent in China.

As is known, the manufacturing cost of cotton textiles in India is comparatively higher than that in Bangledesh and Vietnam. The power cost in India is US cents 10-12 per cent Kwh While it is US cents 9-12per Kwh in Bangladesh and US cents 8 per Kwh in Vietnam. In India the interest rate is 12-13 per cent. Which it is 6-7 per cent in Vietnam, 10-12 per cent in Turkey and 5-6 per cent in China.

As has been reported in these columns earlier, many spinning mills have already turned non performing assets (NPAS), following the stringent norms adopted by RBI. If the current situation continues many more mills may follow suit soon.

An RBI financial stability report (June 2018) shows that the textile sector was amongest the top stressed credit risk industries in the economy. Though its share in total advances of the banking sector is small as compared to infrastructure, the textile industry also exhibits considerable transmission to the banking sector. In addition, the large amounts of reimbursement of funds under TUFS remain pending for a number of claims which is creating financial stress on the industry.

Further more, the government needs to formulate Free Trade Agreements (FTAs) that are industry favourable. The FTAs signed so for are not at par with our competitors as a result of which Indian exporters have to pay heavy duty on their exports making them uncompetitive. The process of concluding FTAs with major markets like the EU, the US and new markets like Australia, Russia etc should be expedited. Efforts should also be made for negotiations with China for reducing import duty on cotton yarn. China is the largest importer of cotton yarn and is also India’s largest export distination for this product.

With excess capacity in the spinning sector there is no need for setting up new units. Therefore, no incentives should be given for the purpose for the next 3 years as that drives existing ones into bankruptcy / non productive assets. The Gujarat Government has taken the lead by not allowing to set up new units and other States must follow suit, except for moderisation of existing capacity.

Next is moderisation of spinning machinery. There are around 15 mn spindles that are 15 years old. In the normal course the machineries need replacement in 7-8 years to produce quality yarn with higher levels of efficiency and productivity.

The continuous increase in Minimum Support Price (MSP) for cotton is a matter of concern for the spinning industry. MSP was increased in 2018-19 by more than 28 per cent and 26 per cent for medium staple and long staple cotton on a year to year basis respectively. With the declining margins of the industry, direct subsidies may be provided to cotton farmers. This will ensure reasonable cotton prices for the industry.

The spinning sector operated 24×7 and draw power at a constant load (925 to 950 units per hour for every MW) while engineering and other sectors may function (only during day and evening time and draw power only) 350 to 500 units per hour for every MW. As the electricity bill is based on the energy consumed, the textile industry deserves to have a lower tariff.